In the previous article we looked at the introduction and classification of financial instruments. It is highly recommended that you check out that article first so that you can have grounded knowledge about what we are going to discuss in this article.

The table shown below, summarizes the classification of financial instruments that was discussed in the last article.

________________________________________

In addition to this the business model and the contractual cash flow test were also discussed in great depth. Which is why starting with the first article on this topic is a good idea. Let us continue where we left off. We covered the methods and basis of classification last time and in this article, we shall look at the measurement of financial instruments and the related complications.

Initial measurement of Financial Assets

According to IFRS 9, the initial measurement of financial assets is on their transaction price, which is also their fair value at the time of making the transaction. However, distinction must be made when the consideration given also includes something other than a financial asset in the transaction. For instance, if the purchase of shares for trading purposes also includes the brokerage costs, then such costs will be excluded from the initial measurement of the shares. The shares in this case will be initially measured at their fair value which should be the market price of shares prevailing on the date of transaction. The difference between the fair value at recognition of shares and the transaction price of shares will be recognized in P&L (Comprehensive Income Statement).

However if the shares are bought for investment and the aim of the business is to collect contractual cash flows and hold the shares, then the shares will be initially measured at their amortized cost and the brokerage costs will be included in the initial recognition.

Subsequent measurement of Financial Assets

According to IFRS 9, financial assets should be classified subsequently at either

• Amortized cost

• Fair value through other comprehensive income (FVOCI)

• Fair value through profit and loss (FVPL)

1. Financial Assets measured at Amortized Cost

Financial assets should be classified at their amortized cost if:

a) Business Model Test: The aim of the business is to hold the assets in order to collect contractual cash flows.

b) Contractual Cash Flow Test:The terms of the financial asset are such that they give rise to cash flows at certain periods that only comprise principle and interest.

This means that assets that are subsequently measured at amortized cost, are those which are held for their contractual cash flows primarily.

The amortized cost of a financial instrument is calculated as

• Amount at initial recognition

• Minus the principal repayments

• Plus/Minus cumulative amortization through the effective interest rate

• Adjusted for loss allowance for financial assets

This can be further understood clearly with a worked example but before we can look at the example, there is a need to clarify what effective interest is.

Effective Interest: Refers to the interest rate that discounts the future payments or receipts over the estimated useful life of the asset or the liability. Consider this as simply the discount rate or the prevalent rate of interest.

Note: Transaction costs are capitalized when financial instruments are measured at amortized cost.

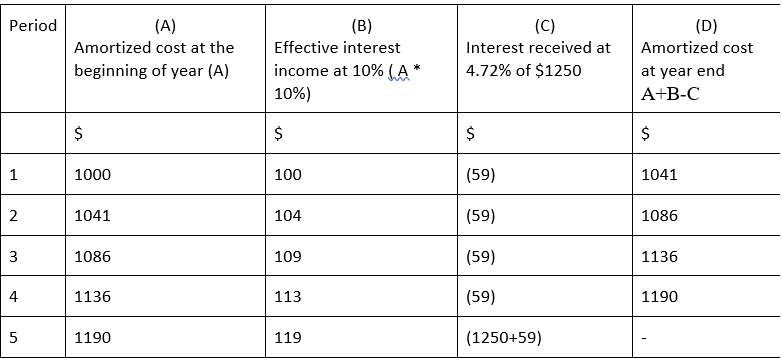

Example1:

Zonko limited purchased a debt instrument at the transaction price of $1000. The instrument has maturity in 5 years’ time, after which Zonko will receive $1250 in principal repayment. The debt instrument has an interest rate of 4.72% and the effective rate of interest is 10%. The aim of Zonko is to collect the contractual cash flows from the instrument. How should the instrument be accounted for in the books of Zonko?

First of all we need to simplify the question to make it easily understandable.

• Zonko purchased a debt instrument for $1000. This is the transaction price and therefore also the initial recognition cost of the debt instrument.

• At the end of term, Zonko will receive $1250 in principal repayment. This means that the actual value of the debt instrument is $1250 and Zonko has purchased the instrument at a discount of $250.

• 4.72% interest is on the nominal value of the instrument, which is $1250. This means that each year Zonko will receive 4.72 x 1250 = $59 interest on this investment.

• $1000 is the initial recognition price and the effective interest will be calculated on this amount. Therefore, the effective interest for this investment should be 1000 x 10% = $100

• The debt instrument will be classified on amortized cost because the business model is to collect contractual cashflows.

In order to make the calculation easy, it is better to make an amortization table.

The amortization schedule shows how the investment into the debt instrument will be valued on a year by year basis in the books of Zonko.

2. Fair value through other comprehensive income (FVOCI)

Financial assets should be classified at FVOCI if

a) Business Model Test: The aim of the business is to not only hold the assets in order to collect contractual cash flows but also to sale the financial assets whether for profit or loss.

b) Contractual Cash Flow Test:The terms of the financial asset are such that they give rise to cash flows at certain periods that only comprise of principle and interest. You may notice that this is the same treatment as for classification at amortized cost.

3. Financial Assets measured at Fair Value through Profit and Loss

Financial assets that cannot be measured at amortized cost or at FVOCI are measured at fair value. The fair value of financial assets is calculated under IFRS 13 which deals with the fair value measurement.

IFRS 13 establishes 3 ways for the measurement of the fair value, these 3 ways are presented in a hierarchy which means that if the first method is not applicable, then the second one should be chosen and so on.

The hierarchy presented in IFRS 13 is as follows

1. Assets should be valued at the quoted price in active markets for identical assets or liabilities at the measurement date.

2. If there is no identical asset or liability in active market to drive the fair value of the asset then quoted prices for “similar” assets and liabilities in active markets should be used, if not this then the quoted prices for identical assets that are not in active market should be used, if not this then other sources should be used to measure the value. The other sources may include interest rates, credit spreads and yield curves. If even this is not possible then market corroborated inputs should be used to measure the fair value of an asset.

3. If the above is not possible then unobservable inputs can be used to measure the fair value. Unobservable inputs include entity`s on data and assumptions about the fair value of the said asset or liability.

Exceptions to Measurement through Fair Value Through Profit and Loss

• Assets that are part of hedging contracts

• Investment into equity instruments that are not held for trading. Such instruments can be recognized in FVOCI if the entity makes an irrevocable choice.

• If the financial instrument is held under FVOCI

Note: Transaction costs are expensed in P&L when the financial assets are held at fair value through profit and loss.

Let us now look at some examples.

Example 2:

Magenta ltd invested in the shares of Forest ltd in February. The total cost of investment into Forest ltd was $800,000. A month later in March, the market price of identical investments was $850,000.

How will Magenta ltd measure this investment initially and subsequently, given that the business model is to collect contractual cash flows?

• Initial measurement of investment into Forest ltd should be at $800,000 as this was the consideration paid for the investment.

• Subsequent measurement in March should be at $850,000 because this is the fair value of the investment according to IFRS 13.

• $50,000 gain will be recognized in Other comprehensive income.

Example 3:

Werewolf ltd invested in 10 million $1 shares of Stag limited at the market price of $5 per share. The transaction cost for the investment was $3 million. At the year end, the share price of Stag limited was at $6.5 and during the year Warewolf limited received 20 cents/share dividend from Stag limited.

Using this information show how Werewolf limited will account for this investment in the following two scenarios

• If the investment was done for the purpose of trading

• If the investment was done to collect contractual cash flows.

Scenario 1

In this scenario, the shares are held for trading and therefore they will be classified on fair value through profit and loss. This means that the $3 million transaction costs will be expensed and the gain on investment at year end will be recognized in profit and loss. The investment at year end will also be valued on the higher fair value.

Werewolf limited will show the following in the Income Statement

• Investment income recognized as gain: $15 million (10m x (6.5 - 5))

• Dividend income: $2 million ($10m x 0.20)

• Transaction costs expensed: $3 million

Werewolf limited will show the following in the Balance Sheet

• Investment in Stag limited: $65 million

Scenario 2

In this scenario the investment into Stag limited will be recognized at Fair value through Other Comprehensive Income. This means that the transaction costs will not be expensed, instead they will be capitalized.

Werewolf limited will show the following in the Income Statement

• Dividend income: $2 million ($10m x 0.20)

Other comprehensive income

• Investment income recognized as gain: $15 million (10m x (6.5 - 5))

Werewolf limited will show the following in the Balance Sheet

• Investment in Stag limited: $68 million (65+3)

Initial measurement of Financial Liabilities

According to IFRS 9, the initial measurement of financial liabilities is done on their transaction price which is also their fair value at the time of making the transaction. However, distinction must be made when the consideration given also includes something other than a financial liability in the transaction. In this case the financial liabilities are measured in a manner like financial assets, as stated above.

If the financial liability is going to be treated at the amortized cost, then the treatment for the financial liability will differ from that of financial assets. For a financial liability to be recognized at amortized cost, the transaction costs will be deducted from the transaction cost.

For example, if the purchase of debentures includes the transaction costs then these transaction costs will be deducted from the value of debentures payable and then the debentures will be recognized. if a company issues debenture worth $1 million and this issue price includes 5% transaction and issuance costs then the debentures will not be recognized at $1 million which is the transaction price. The debentures will instead be recognized at $950,000.

Subsequent measurement of financial liabilities

According to IFRS 9, financial liabilities should be classified as follows

• At amortized cost

• At fair value through profit or loss

Financial liabilities measured at amortized cost

The measurement for financial liabilities on amortized cost is the same as that of financial assets that we have covered above. The only difference is that for financial liabilities the transaction costs are expensed instead of being capitalized.

Example 4:

Stellar co issues a bond on deep discount at $503,778 for a term of 3 years. The bond does not carry any interest and its redemption value is $600,006. The effective interest rate of the bond is 6%.

Difference between the final amortized cost at the end of year end is due to rounding.

Deep discount bond means that the actual value of the bond is $600,006 which will be payable to the bond holders at the end of the term but the bond has been issued at a discount of $96,228. So although the bond does not pay interest to investors, the discount of $96228 can be considered as financing element in the bond that has been incorporated through the deep discount. This discount has to be spread out over the bond term

Stellar co will record $30,226, $32,040 and $33,962 as the finance cost in the profit and loss account for the respective years and the values $534,004, 566,044, 600,006 will appear as the outstanding balance at year end for the relevant periods.

Example 5

Crackers limited issued $600,000 worth of debentures on 1st January 2020. The issue cost was $200, which was included in the $600,000 figure. The debenture does not carry any interest rate but the effective interest rate is 12%. The term of debentures is 2 years, which means that the debentures can be redeemed in 2022 at a premium of $152389.

This is an interesting question. The debentures do not carry any interest rate but if you look at the details you can see that the debentures are redeemable at a premium of $152389. This means that the debentures were issued at $600,000 but at their redemption Crackers limited will have to pay $752,389. The premium therefore acts as a financing component and this cost must be spread over the life of the debentures.

The calculation can be made simpler by the use of an amortization table.

This table shows that the finance cost for each of the two years will be $71976 and $80613. It is also important to note that the debentures were issued for $600,000 and this amount is inclusive of issuance costs, therefore the financial liability will be recognized after subtracting the cost of issuance.

Financial liabilities measured at Fair Value through Profit or Loss

When financial liabilities are held for trading, they are revalued annually according to IFRS 13, which we have covered above. There are however certain exceptions.

Exceptions

(a) If the financial liabilities are a part of hedge

(b) If the financial liability is classified as FVPL and the company is required to disclose the effects of changes in the financial liability`s “Credit Risk” in Other Comprehensive Income in the Income Statement.

What is Credit Risk?

Credit risk refers to the risk of loss resulting from the borrower’s inability to repay a debt or the risk that the lender may not receive the principal and interest that has been lent out.

According to IFRS 9, financial liabilities classified as FVPL must classify their gain or loss into

• Gain or loss arising from credit risk

• Gain or loss arising from other categories

IFRS 9 introduced this requirement because when a financial liability is measured at fair value, this means that the fair value of that financial liability can increase or decrease. Now this is a normal thing to happen. Consider the example that a company issues bonds to finance capital expenditure. The nominal value of the bonds is $1 million on the date of issue and the bonds carry variable interest. A few months later the interest rates increase, causing the bonds to fetch a higher interest rate and as a result the fair market value of bonds increases. Although the par value of bonds is $1 million but their fair value is higher than this. This is a gain that needs to be shown through profit and loss.

Similarly, if the interest rate drops and the fair market value of the bonds drop, causing the fair market value to become $800,000 instead of $1 million. This would cause a loss, and this will need to be classified through gain or loss arising from other categories. This is not a credit loss.

However, consider the situation where a company issues bonds and they are rated as AAA bonds by credit rating agencies. A quarter later, the company runs into financial difficulties and its liquidity drops. As a result the credit rating agencies downgrade the investment grade AAA bond into BBB rated bond. This downgrade would also affect the fair market value of the bond, which would fall. Investors will be less willing to invest into the bonds of a company that has just been downgraded.

This loss in fair value would be classified as a credit loss. The opposite can also happen, where the fair value may rise if a company is upgraded from BBB to AAA, thus resulting in a credit gain.

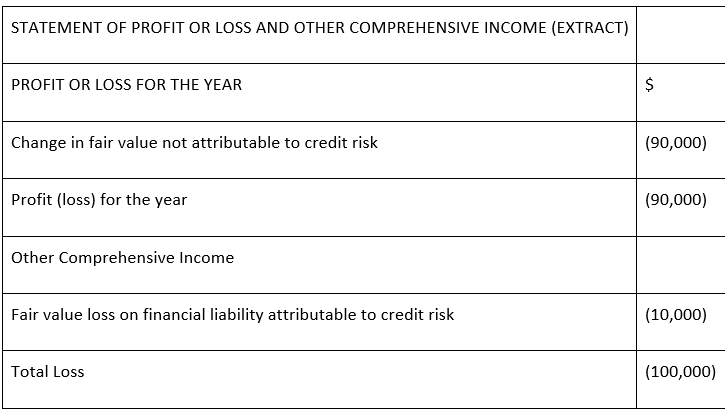

Credit loss must be reported in Other Comprehensive Income to differentiate it from loss arising on a financial liability due to other reasons. The reason for this differentiation is simply to make the financial statements less confusing.

Let us look at an example.

First let us assume that IFRS 9 does not require credit risk to be disclosed in other comprehensive income. A company has suffered from a loss in fair value of its financial liabilities by $100,000. This figure includes both credit loss and other losses. But since there is no requirement to show credit loss separately, this loss would be disclosed as.

Before IFRS 9, users of financial statements found this presentation confusing, which is why IFRS 9 proposed the following presentation.

Hopefully, this article has made the classification and then the initial and subsequent measurement of financial instruments clearer. This is a complicated area and once a IFRS Dip student or professional has understood the principles the only way to improve understanding of these concepts is to carry out as much practice as possible to reinforce these concepts.