As we discussed in the previous article, the need for a new model for the impairment of financial instruments arose after the 2008 financial crisis, although it took almost a decade for the standard to be made and implemented, it is finally operational and now entities are required to follow the new model to take into greater account the risk that the financial instruments are exposed so.

By embedding risk, it has been made sure that the financial instruments are presented in a more realistic manner. The impairment model given in IFRS 9 is therefore based on measuring the expected credit losses.

The expected credit loss model tries to effectively include the risk of default for financial instrument before it is incurred. As such, the default may not occur, but this approach is like the concept of provision for doubtful debts or the provision for warranty, where the provision is maintained by estimating the risk of loss.

That loss may never occur, the debtors may pay back in time and there may not be any need for legal claims but in the chance that they do occur, the provisions have already taken this risk into account. Expected credit loss model therefore follows this line of thought when it comes to financial instruments.

Key Definitions

Let us first look at some of the key definitions before proceeding further.

Credit loss: The expected shortfall in contractual cash flows. (IFRS 9)

Expected credit losses: The weighted average of credit losses with the respective risks of a default occurring as the weights. (IFRS 9)

Lifetime expected credit losses: The expected credit losses that result from all possible default events over the expected life of a financial instrument. (IFRS 9)

Past due: A financial asset is past due when a counterparty has failed to make a payment when that payment was contractually due. (IFRS 9)

Purchased or originated credit-impaired financial asset: Purchased or originated financial asset(s) that are credit impaired on initial recognition. (IFRS 9)

Credit-impaired financial asset: A financial asset is said to be credit impaired when one or more events have occurred that have a detrimental impact on the estimated future cash flows of that financial asset. (IFRS 9)

Indictors of Impairment under IFRS 9

According to IFRS 9, a financial instrument is said to be impaired if all or any of the following indicators are present

• The issuer of the financial instrument encounters severe financial difficulties.

This would mean that the principal and interest portion of the financial liabilities are at the risk of not being paid.

• If the breach of contract occurs, this means that if the principal or interest payments cannot be paid off.

• If the lender allows a significant concession to the borrower. The nature of the concession being such that it would not be considered under normal conditions and thus only exists because the borrower has encountered a financial difficulty.

• The bankruptcy of the borrower becomes probable.

• The active market for the financial instrument in question disappears.

• Purchase of financial asset on deep discount. The deep discount in this case reflects the credit losses inherent in the financial asset. The issuer of the financial asset had to offer a deep discount to attract investors, who otherwise would not have invested in the financial asset.

Impairment may be caused by the occurrence of any one or more of these indicators.It is not always easy to distinguish between these indicators and thus more than one of these indicators may occur in order for a financial instrument to be considered as impaired.

Expected Credit Loss Model

The expected credit loss model is a new model that was previously not present in IAS 39. IAS 39 used the "incurred loss" model which meant that financial instruments such as loans would only stand impaired if any event occurred that would trigger impairment. In the absence of any such trigger, the loan would be repaid without any risk.

This simply meant that until and unless the loan defaulted, it could not be impaired in the books. The 2008 financial crisis raised a lot of concerns regarding this model of IAS 39 as the model clearly failed to account for the deterioration in the quality of credit that was happening quite some time before the financial crisis. If you would like to explore more details about the financial crash at 2008, there is one article written about that in IFRS blog, CLICK HERE

Had the IAS 39 been more forward looking, it would have indicated the oncoming crisis by the increased impairment of financial instruments in the books of corporations. One of the biggest criticisms of the IAS 39 incurred model approach was that it resulted in overstated interest particularly before the loss occurs.Thus, giving the shareholders and management a false sense of confidence in the financial strength of the company.

IFRS 9 takes the expected credit loss approach, which is a more forward looking and prudent approach and it looks at the general increase or decrease in the credit quality of the financial instruments in question.

Expected credit losses are calculated by considering the cash shortfall that are expected to occur under a variety of default scenarios. The shortfalls in cash under different scenarios are then multiplied by the probability of each scenario to arrive at the expected credit loss figure. The final figure for the expected credit losses is the sum of all the probability weighted outcomes.

Risk is inherent to every financial instrument and for this reason, expected credit loss is inherent in every financial instrument from its inception. It is important to understand that expected credit loss is not an economic loss as it has not occurred yet. In that regard it is a provision or an allowance, as discussed in the introduction.

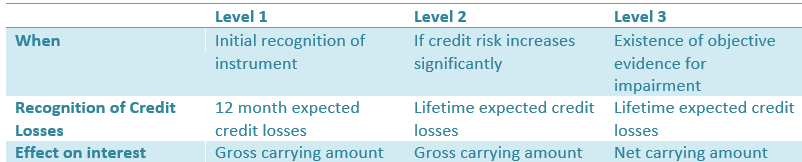

IFRS 9 has three different levels for the measurement and recognition of expected credit losses.

• The first level is applicable on financial instruments whose quality has not yet significantly deteriorated since their initial recognition. The impairment for instruments at this level is comprised of the present value of expected credit losses for the next 12 months. Interest revenue for financial instruments at stage one is calculated on gross carrying amount of the financial instruments.

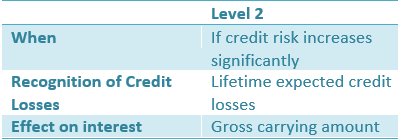

• The second level applies to assets whose financial quality has deteriorated significantly since their initial recognition. The impairment for instruments as this level is comprised of lifetime expected credit loss. The gross carrying value of the financial instruments should be reduced by lifetime expected credit loss for the periods where there is no expectation of reasonable recovery in value. Interest revenue for financial instruments at stage one is calculated on gross carrying amount of the financial instruments.

• The third level is for financial instruments for which there is objective evidence of impairment on reporting date.The impairment for instruments as this level is comprised of lifetime expected credit loss. The gross carrying value of the financial instruments should be reduced by lifetime expected credit loss for the periods where there is no expectation of reasonable recovery in value. Interest revenue for financial instruments at this stage is recognized on the net carrying amount (Gross carrying amount minus lifetime expected credit loss).

IFRS 9 also recognizes that there are certain financial instruments that will have low or very low credit risk and these instruments will not meet the criteria for lifetime expected credit losses. Such instruments are not required to be treated for impairment as these are deemed to be investment grade instruments with very low default risk.

Objective of the IFRS 9 impairment model

We have already discussed this before, simply reiterating the already discussed information here for clarity.

The objective of impairment of financial instruments in IFRS 9 is to recognize the expected credit losses, which are simply the expected short fall in the contractual cash flows of a financial instruments. It is important to understand that when we impair noncurrent assets, we look at the fair values which indicate that the loss or gain in the fair value has already occurred in the market and the entity simply has to restate the fair value of the non current asset.

When it comes to financial instruments, we are no longer following the incurred model. Therefore the losses that we will be looking at are not incurred losses instead they are the expected losses and as such have not yet occurred. The expected losses are based on the risk profile of the financial instruments and carefully calculated probability, which is then applied on the value of the financial instrument.

Scope of IFRS 9 for Impairment of Financial Instruments

IFRS 9 applies the expected credit losses model to the following

• Financial assets measured at amortized cost

• Financial assets measured at FVOCI mandatorily

• Loan commitments that do not have any obligation to extend credits. Exception to this rule are loan commitments that are measured at FVPL

• Financial guarantee contracts under IFRS 9.Exception to this rule are contracts that are measured at FVPL

• Lease receivables

• Contract assets under IFRS 15

Basic Principle

The expected credit losses should be based on information that is available to the entity in a reasonable manner, without requiring unreasonable cost or effort. The information can comprise of historical data, current data, and financial projections for future periods.

The figure for expected credit losses should be updated for any change or new information and expectations in each reporting period based on the data available to an organization.

For example, a company invests in the bonds issued by another entity. According to due diligence carried out before investment the bond issuing entity was rated AA and had stable financial fundamentals. The bond has a term of 4 years and was thus initially recognized as an investment grade bond with very little risk of default.

2 years later, the investing company finds out that the bond ratings have been deteriorated to BBB by credit rating agencies. This means that the initial assumption of the company is now obsolete and if there is significant indication of impairment then the bond should be classified at stage 2.

Measurement of Credit Loss on initial recognition

A credit loss provision or allowance should be created that is equal to 12 months expected credit losses. The calculation for this is quite simple. The probability of the default in next 12 months is multiplied by the lifetime credit losses to arrive at the credit loss provision for 12 months expected losses.

Subsequent years

Subsequent measurement of the impairment is as follows. If the credit risk on the financial instrument increases by a considerable amount as compared to the initial recognition, then the amount initially recognized shall be replaced with "lifetime credit losses". If in due course the credit risk improves then the lifetime credit losses can be reversed and initially recognized expected credit loss should be reinstated.

Let us now have a look at an example to reinforce our understanding so far.

Example 1

Assume that a bank has lot of clients from the textile industry among other clients.

The bank mainly provides mortgages and loans to its clients, the loan to value ratio of the bank is quite high at 80%. The applicants are required to provide detailed background information before the loan can be approved such as

• Business credit rating

• Bank statements

• Tax returns

• Recent financial statements

The bank uses this information to gauge the financial viability of the clients before approving any loan or mortgage. The bank also secures the loans or mortgages with the property in question.

After the roll out of IFRS 9, the bank has adopted the standard and it now measures all financial instruments based on IFRS 9 and thus applies the expected credit loss model.

As a part of normal operations to collect information on the financial viability of clients, the bank has found out that the textile industry is struggling to compete with the international competitors that have recently entered the market.

This has resulted in a significant reduction of revenue and profitability as many clients of the bank have lost their market share to international competitors.

Under the given conditions, how should the bank apply IFRS 9?

The bank should firstly separate the portfolio of clients belonging to the textile sector. This portfolio is the one that is facing impairment now.

Once the portfolio has been identified and separated, now the bank needs to see the extent of loss that the industry is facing. From the information that hasbeen supplied, it seems that thereis a significant risk of credit losses due to the threat of international competitors. The portfolio of the textile industry clients seems to be in the second stage, as identified in the table below.

The bank should therefore recognize lifetime credit losses and reduce the value of financial instruments that are due. The interest income should continue to be calculated on the gross carrying amount.

While estimating the expected lifetime credit loss, the bank should consider recoverable money through the collateralized assets. The existence of collateral in this case acts as a failsafe mechanism because the value for lifetime credit losses is going to be significantly low because of the collateral, even though the entire portfolio is categorized in stage 2.

As the time progresses the bank compiles more data and is now able to identify clients that defaulted or were going to default in near future. Recognizing this development, how should the bank proceed?

The actions of the bank will depend on the extract of the table presented above. There is now objective evidence available for the impairment of specific clients. This means that lifetime credit losses should continue to be recognized. The interest income however will now be calculated on the net carrying value.

Example 2

A bank has approved $20 million overdraft facility for a portfolio of clients. The funds have not yet been withdrawn from the overdraft facility. According to the bank

• $18 million of the total overdraft facility can be classified as stage 1. Out of the $18 million, $9 million are expected to be withdrawn in the next 12 months. The probability of default is 2% over the 12 month period.

• The remaining $2 million is classified as stage 2 and is expected to be fully withdrawn over the remaining life. The probability of default is 20%.

This means that a credit allowance of $580,000 will have to be recognized by the bank against the overdraft facility.

Recognition of Impairment

Although this has been mentioned above under the scope of IFRS 9 heading, but it needs to be repeated for clarity. In all three of the stages the credit losses need to be recognized in profit and loss as credit allowance. This credit allowance is to be held separately, which means that it cannot be merged with any other allowance, it must be shown as a separate allowance.

Adjustment of loss allowance

As mentioned above, the credit loss needs to be updated at year reporting period. This means that the value of the credit allowance will move up or down at each reporting period. Any impairment gain or loss is to be recognized in the profit or loss, followed by any subsequent adjustment.

Presentation

Credit losses for all three stages are recorded in the profit and loss statement (SOCI) and offset against the carrying amount in SOFP. Except for debt investments classified at fair value through OCI.

Investments in debt classified at OCI have a slightly complex adjustment. As we have studied before, instruments carried at fair value through OCI have to differentiate between credit losses and losses through other means.

Any loss or gain due to credit loss, needs to be recognized in the profit and loss and any gain or loss due to any other reason must be recognized in OCI. In this case no credit loss allowance is required as the asset is automatically adjusted at fair value.

Purchased or originated credit-impaired financial assets

Sometimes it happens that certain financial assets are credit impaired from their inception. For instance, a company offering deep discount bonds, is effectively offering credit impaired financial assets. Thus,financial assets that are credit impaired from their inception or acquisition should be considered at stage 3 from the beginning.

Therefore, changes in lifetime expected losses for such financial assets should be recognized from the time they are recognized by an entity and a loss allowance should also be recognized with initial recognition, with changes going to profit or loss. Any future gain would be classified as reversal of impairment loss.

This concludes our series of articles on IFRS 9, it is without any argument a very complex standard and one must keep analyzing and studying (if you are IFRS DIP student) the standard over and over again in order to reinforce the concepts that have been introduced in it.