IFRS 9 - Financial instruments is a relatively new financial standard that has recently replaced the older IAS 39 - Financial instruments. The new standard has been applicable since 1st January 2018, however some entities that predominantly have to deal with insurance related activities have the option of delaying the adoption of the new standard till 2021.

If you are a student or a young professional, then the very mention of IFRS 9 may make you worried. IFRS 9 is generally seen as a complex financial standard, which is true because it deals with the advanced concept of categorizing and measuring financial instruments. In this article, we shall try to simplify the concepts contained in this standard and present the complications in such a manner with little practices, you can feel confident while tackling issues related to this standard.

What is a Financial Instrument?

The term financial instrument relates to any contract that gives rise a financial asset of one entity and financial liability or equity instrument of another entity.

What is a Financial Asset?

The term financial asset refers to any asset that is

• Cash

• Equity instrument of another entity, for example shares of another company.

• A contractual right to receive cash or another financial asset from another entity (For example receipt of cash for the sale of goods (i.e. accounts receivables); or to exchange financial instruments with another entity under conditions that are potentially favorable to theentity

A contract that will or may be settled in the entity's own equity instruments and is:

o A non-derivative for which the entity is or may be obliged to receive a variable number of the entity's own equity instruments. For instance, a contract to receive a bond in exchange for a certain number of shares of the company. In simply words instead of investing into the bond with cash, a company may decide to issue shares to purchase the bond with.

o A derivative that will or may be settled other than by the exchange of a fixed amount of cash or another financial asset for a fixed number of the entity's own equity instruments. This refers to a derivative contract that is settled by issuing shares of the entity. For example, if a company enters a call option for $50,000 in exchange for its own shares.

What is Equity Instrument:

The term equity instrument has been mentioned in the definition and there is a need to clarify it. Equity instrument refers to any instrument that gives its bearer the right to the assets of the company after deduction of its liabilities. In simple words equity instrument refers to shares.

Some of the financial assets according to the above-mentioned definition are

• Trade receivables or debtors

• Options

• Shares, only when they are categorized as investment

What is a Financial Liability

• A contractual obligation:

o To deliver cash or another financial asset to another entity (i.e. accounts payables), or

o To exchange financial instruments with another entity under conditions that are potentiallyunfavorable; or

• A contract that will or may be settled in the entity's own equity instruments and is:

o A non-derivative for which the entity is or may be obliged to deliver a variable number of the entity's own equity instruments. For instance if a company decides to issue bonds and in return for cash, it instead settles for the shares of the entities buying the bond.

o A derivative that will or may be settled other than by the exchange of a fixed amount of cash or another financial asset for a fixed number of the entity's own equity instruments. This may sound similar to what is in the definition of assets above but a derivative classified as a financial liability refers to a derivative with its fair value in the negative position.

Some of the financial liabilities according to the above mentioned definition are

• Trade payables or creditors

• Debentures: Debentures are unsecured debt instruments that carry interest, similar to bonds.

• Redeemable preference shares

• Forward contracts currently at loss

What is a Derivative?

Derivatives are financial instruments and according to IFRS 9, to be classified as a financial instrument a derivative must have all three of the following

1. The value of the derivative must change in response to the interest rate, its own security and commodity price, the forex rate or any other similar variable that affects it. For instance, one variable that affects the price of oil futures is market demand. One variable that affects the price of gold futures is market risk, if the market risk goes high the price of gold futures increases. So, a derivative is an instrument whose price changes due to any change in its variable.

2. A derivative requires little or no initial investment at all. Futures and options do not require initial heavy investment, the only investment is the premium which is only a fraction of the total contract price.

3. The derivative must be settled at a future date.

Some examples of derivatives are

• Forward contracts

• Future contracts

• Options

• Swaps

Reminder:

Financial instruments include primary instruments for instance receivables, payables and equities. Derivatives which are secondary instruments are also included in financial instruments.

At this point it is especially important to understand which assets are not financial instruments. Many students and professionals mix these up. If you cannot exactly remember which instruments are financial instruments according to the above-mentioned definitions although it is very easy to, then just remember the following instruments, which are not financial instruments.

• Physical assets

o Inventories

o Property, plant, and equipment

o leased assets

• Intangible assets

o Patents

o Goodwill

o Trademarks etc

• Prepaid expenses

• Deferred Revenue

• Assets and/or liabilities that are not contractual in nature

• Contractual rights/obligations that do not require future transfer of financial assets for instance operating leases.

Note:

If you look at the definition of financial instruments again, then you will see that contingent assets and liabilities are also fulfilling this definition, so that would make them financial instruments as well.Contractual rights exist for contingent assets and liabilities because of past transactions. However contingent assets and liabilities may not meet the recognition criteria, as their recognition requirements are covered under IAS 37 which is a separate standard.

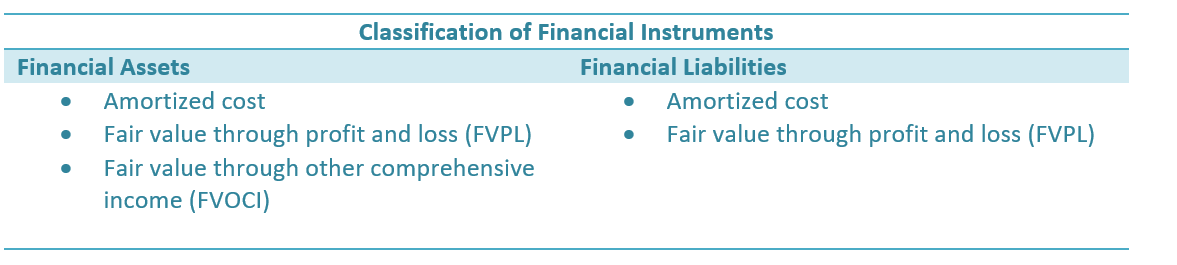

Classification of Financial Instruments

There are many different aspects of IFRS 9 but for the time being we are going to limit ourselves to the "Classification and measurement of financial assets" portion of the standard as this portion is both new and complicated to understand.

According to IFRS 9, financial instruments should be classified at either

• Amortized cost

• Fair value through profit and loss (FVPL)

• Fair value through other comprehensive income (FVOCI)

To simplify the matters further, have a look at the following table

Classification of Financial Instruments

We shall look at the above-mentioned classifications in further detail later. Let us first focus on the basis for these classifications

These are the three different classifications within which the financial instruments can be classified. The basis for these classifications is made on two factors which are

1. The business model of the entity for managing financial assets

2. The contractual cash flow characteristics of the financial assets

Business Model Test

The business model refers to how the entity intends to use the financial asset. For instance, if a company has invested into the shares of another company, this investment in shares can be seen in different ways. It can either be considered as equity investment where the entity in which investment has been done can be classified as an associate or subsidiary.

The investment can also be seen as investment done only for the purpose of benefiting from the movement in share price. So, the purpose for which the entity has invested will determine how the financial assets will be categorized.

The contractual cash flows also need to be considered. Debt instruments like debentures have cashflows that occur on specific dates whereas dividends do not occur on specific dates. The treatment for both therefore will be quite different.

IFRS 9 has also defined that the classification depends upon the company. A company may hold some financial assets for trading and some for collecting contractual cash flows. In this situation, the classification must be done on the portfolio level. However there may be a situation where a company has classified a financial asset for trading but then that asset loses its market value but it still carries contractual cash flows and so the company may decide to classify it based on its cash flows.

Therefore, what we can conclude from this is that:

• The decision for "business model test" is made based on how the management manages the business.

• A company can have more than one business model for its financial assets. As mentioned above, if there are many financial assets that a company owns, it may decide to hold a certain number of financial assets in a portfolio as held for contractual cash flows and another certain number of financial assets in another portfolio as held for trading. It would therefore be appropriate for the entity to carry out assessment for classification purposes at the portfolio level, instead of the entity level.

It must be remembered that setting a business model is not like choosing whether to use Cost Model or Reevaluation model for noncurrent assets. In the case of noncurrent assets, if one model is chosen then it must apply on the whole category. Whereas for financial instruments the business model can differ with each instrument.

• Lastly, while a business may classify financial assets as being held for contractual cash flows, but it is not necessary to hold them till maturity.

Let us now look at some examples to further clarify this new concept which has been introduced in IFRS 9 and was not previously a part of IAS 39.

Examples

The following examples, from the Application Guidance to IFRS 9, are of situations where the objective of an entity’s business model may be to hold financial assets to collect the contractual cash flows.

Example 1

Xander Corp holds financial investments to collect their contractual cash flows but the company also has a policy of selling the investments in certain exceptional circumstances. For example, the company may sell the investment if its credit rating drops too low.

Looking at this situation, it can be said that Xander Corp should classify the financial investments as held for contractual cash flows and not for trading.

Why? Because the primary objective is to hold these investments unless exceptional circumstances arise.

However if the sales of these financial instruments becomes frequent then the company will have to change its classification and must hold the instruments as held for trade, because then the treatment of the investments would not be in line with the stated objective of collecting contractual cashflows.

Example 2

Galaxy limited is in the business of originating loans, the loans are then sold to a securitization company which is also a subsidiary of Galaxy limited. the securitization company issues financial instruments backed by the contractual cash flow of the loans. The financial instruments are bought by Galaxy limited.

How should the loans be treated?

First of all here we need to understand that we are dealing with both consolidation and financial instruments. In the separate financial statements, Galaxy limited will classify the originated loans as held for sale because the primary objective is to originate loans and then sell them. Whereas the subsidiary securitization company will classify the loans as held for contractual cash flows.

The consolidated group will also recognize the financial instruments as held for contractual cash flow because the sale is only made on the intra group level and thus eliminated. The primary objective of the group is therefore to collect cash flows from the loans.

Example 3

Kalvin limited has a portfolio of financial instruments that vary in their credit rating. The business objective is to collect contractual cashflows, however some of the instruments with low ratings do not return the contractual cash flows and Kalvin limited has to use debt collecting agencies or sell the instruments under exceptional terms in order t liquidate the bad investments.

Kalvin limited should recognize the financial assets as held for contractual cash flows. This is quite straight forward, even if the contractual cash flows cannot be recovered due to high risk or illiquidity of the instruments, it still does not change the primary objective of the company. Similarly using debt collecting agencies does not change the primary objective which is to hold the financial instruments for their cash flows and not for trade.

Contractual Cash Flow Test

IFRS 9 requires the contractual cash flows of the assets to be assessed in order to be classified appropriately. IFRS 9 has introduced the concept that only those financial assets which have contractual cash flows in the form of principle and interest, shall be measured on Amortized cost basis. All other financial assets are to be measured at FVOCI or FVPL.

Going by this explanation, if we look at convertible loan stock, then we can see that although the loan part of convertible loan carries principle and interest on principle but the convertible option means that there is a possibility of being converted into shares and therefore for this reason convertible loan stock cannot be measured on Amortized cost basis.

It must be remembered that to be measured on Amortized cost, the financial instrument must carry a principal and interest on that principal. The interest can either be fixed or variable or a combination of both. Bonds and other interest-bearing instruments for instance carrying fixed or variable interest rates can be measured at amortized cost.

Let us now look at some more examples to clear this concept further.

Example 4

Enterprise limited, will have to incur capital expenditure in 10 years’ time and to generate funds for this, Enterprise ltd invests excess cash into short term investments. The business model is to collect cash from the cash inflows. When the short-term investments are close to maturity Enterprise ltd sells them and reinvests the cash into more short-term securities, collecting their cash inflow till their maturity and this cycle is repeated for ten years. At the end of ten-year term, Enterprise ltd will sell the investments to fund the capital expenditure.

How should the short-term investments be classified?

The business model of Enterprise ltd is to collect contractual cash flows, so this is how the short-term investments will be classified.

Selling these investments before maturity is only incidental to the nature of these investments and Enterprise limited does not have a stated policy of selling or trading the securities, therefore the business model is to collect contractual cash flows.

Let us consider these classifications in further detail now.

Classification of Financial Assets

According to IFRS 9 financial assets should be classified as follows

• Amortized cost

• Fair value through profit and loss (FVPL)

• Fair value through other comprehensive income (FVOCI)

Classification at Amortized Cost

Financial assets should be classified at their amortized cost if

a) Business Model Test: The aim of the business is to hold the assets to collect contractual cash flows.

b) Contractual Cash Flow Test: The terms of the financial asset are such that they give rise to cashflows at certain periods that only comprise of principle and interest.

It is important to note here that "equity instruments" cannot be measured at amortized cost. Equity instruments such as shares do not meet the contractual cash flow test. One requirement of the contractual cash flow test is that the assets must have cash flow arising on specific dates. The dividend income on shares, does not have this restriction. The declaration of annual or interim dividend is at the discretion of the company and dividend payment can be skipped or delayed, which means that shares do not have cash inflow at specific dates.

Another condition of the contractual cash flow test has been discussed above. The financial asset in question must carry principle and interest on that principal. Since equity instruments do not pass these two tests for contractual cash flows they therefore cannot be measured on Amortized cost.

Classification at Fair Value through Other Comprehensive Income

Financial assets should be classified at FVOCI if

a) Business Model Test: The aim of the business is to not only hold the assets in order to collect contractual cash flows but also to sale the financial assets whether for profit or loss.

b) Contractual Cash Flow Test: The terms of the financial asset are such that they give rise to cash flows at certain periods that only comprise of principle and interest. You may notice that this is the same treatment as for classification at amortized cost.

Classification at Fair Value through Profit or Loss

Any financial instrument that cannot be classified according to the above mentioned 2 classifications, should be measured as fair value through profit or loss.

Reclassification of Financial Assets

Reclassification is only permitted when there is a valid change of business model. If there is no change of business model, then reclassification cannot be permitted. For instance, if the business has invested in financial assets and the said financial assets lose their market value, so now the business cannot reclassify the assets for trade if they were previously held for contractual cash flows.

IFRS 9 allows financial assets to be reclassified from

• Amortized cost to Fair Value

• Fair Value to Amortized Cost

•Amortized Cost to Fair Value

If the financial asset is reclassified from amortized cost to fair value, then there can be two possibilities. The fair value can either be higher than the amortized cost or it can be lower. Any gain or loss needs to be recognized in profit or loss.

•Fair Value to Amortized Cost

If the financial asset is reclassified from Fair Value to Amortized cost, then the fair value on the date of reclassification shall be considered as the carrying value of the financial asset.

Classification of Financial Liabilities

According to IFRS 9, financial liabilities should be classified as follows

• At fair value through profit or loss

• Amortized cost

Classification at Fair Value Through Profit or Loss

Financial liabilities should be classified at fair value through profit or loss if

• They are held for trading

• At initial recognition they are classified at fair value through profit or loss.

Derivatives must always be measured at fair value through profit or loss.

Classification at Amortized Cost

All financial liabilities not classified at FVPL to be classified on amortized cost.

For this article, let us keep it till here. The next one shall look at further complexity of measuring financial instruments. Since this is a very complex topic, it would be better to go through this article more than once to make sure that your concepts are clear before moving on to the next one, where we shall look at some calculations and more advanced concepts.