Consolidation of

Financial Statements |

Part 5

We have so far covered in detail the rationale behind preparing the consolidated financial statements and the various complications that arise upon consolidating the SOFP for a group. This article shall be the last one to cover SOFP complications as we have discussed lost all of the major complications that arise. Those that are left shall be discussed in this article.

So if you haven`t read the previous articles, it is highly advised that you do so before continuing on with this one.

The last article discussed the treatment of acquisition of internally generated intangible assets and the fair value adjustments upon acquisition.

In this one we shall discuss the treatment of intra group transactions relating to non current assets and mid year acquisitions, to finally wrap up our discussion on SOFP consolidation.

Consolidation Complications - Transfer of Non-Current Assets

It is common among group companies to transfer non current assets to each other. From the individual companies point of view this transfer happens in the form of a sale from one company to another which is totally valid from one company to another, this is a routine transaction where one company sells a non current asset to another company for a profit or a loss.

The buying company receives the non current asset and records it at its price and then starts depreciating it from this date, based on the new price.

If you have been following the previous articles, you will now realize that there is going to be problem when it comes to consolidating the financial statements of companies that have carried out transfer of noncurrent assets in this manner.

As far as the group is concerned hence no transfer has occurred, which means that the effects of the transfer will have to be eliminated and the group statements will need to show the asset as it originally was before the transfer.

The following adjustments will need to be made.

• Profit or loss will need to be removed from the books of the company that made the sale.

• Depreciation charge will need to be corrected in the books of the company that made the purchase. This is an important point to understand.

We are not going to completely reverse the transaction because the title of the asset has passed on. Instead we will simply adjust the depreciation to be how it should have been if the transfer had not taken place.

Carrying out these two transactions will bring the transferred non-current asset back to its original cost less accumulated depreciation value for the group. Although carrying out these adjustments is going to be quite straight forward but it must be remembered that we are working with consolidation which means that each adjustment is going to have its effect on other items as we have seen before.

The most notable effect is going to be on the NCI, which can be summarized as follows.

• In case that the sale of noncurrent asset was made by the subsidiary to the parent, the NCI will share the adjustment of profit/loss.

• In case that the sale of noncurrent asset was to the subsidiary from the parent, the NCI will share in the adjustment of depreciation.

Let us now look at this with a worked example, to better understand how these transactions are to be made.

Example 1

Assume that P owns 80% of S

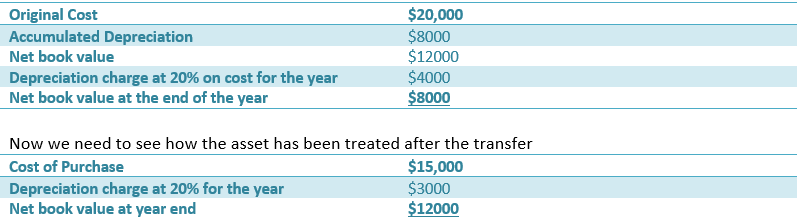

An asset was transferred within the group at the price of $ 15000 on 1 January 20X0. The original cost of this asset was $20,000 and the accumulated depreciation till the date of transfer was $8000.

The group policy is to depreciate all assets at 20% on cost to the company, recognizing full years depreciation in the year of purchase and non in the year of sale.

Adjust this transaction for consolidation if

• The sale was from Parent to Subsidiary

• The sale was from Subsidiary to Parent

Firstly, we need to see what the original entries would have been had the transaction not taken place.

This was a simple working. Now we need to reverse the sale and make adjustment as if the sale never took place, for this we will need to

• Reverse the profit on sale. The NBV of the asset was $12000 and it was sold for $15000, which means that $3000 profit was generated, which needs to be reversed in the books of company that made the sale.

• The depreciation charge should have been $4000 for the group but it has only been shown as $3000, so depreciation charge needs to be increased by $1000 in the books of the company that made the purchase.

• Finally the net book value of the asset should be $8000 and it is appearing as $12000, so the net book value needs to be reduced by $4000 to $8000 in the consolidated SOFP.

Scenario 1: Sale from Parent to Subsidiary

So now let us look at the first scenario that the sale was made by the Parent to the Subsidiary.

This means that the NCI will only share the depreciation adjustment.

• The profit in the income statement of the parent will have to be reduced by $3000.

• The depreciation charge in the books of the subsidiary will be increased by $1000, thereby reducing the profit by $1000. The total effect of first two transactions is therefore $4000.

• The asset will be decreased by $4000 in the statement of financial position. So the overall impact will be nil, but these adjustments have to be made for the purpose of consolidation.

• Since the asset has been purchased by the subsidiary, NCI will take the effect of increase in depreciation by $1000. Which means that NCI will reduce by $200 ($1000 x 20%)

Scenario 2: Sale from Subsidiary to Parent

If the transfer was from subsidiary to parent then the following adjustments would be made

• The profit in the income statement of the subsidiary will have to be reduced by $3000.

• The depreciation charge in the books of the parent will be increased by $1000, thereby reducing the profit by $1000. The total effect of first two transactions is therefore $4000.

• The asset will be decreased by $4000 in the statement of financial position. So the overall impact will be nil.

• Since the asset has been purchased by the parent and sold by the subsidiary, NCI will take the effect of elimination of the profit on sale by $3000. Which means that NCI will reduce by $600 ( $3000 x 20%)

Hopefully have been following this series on consolidation of financial statements and by now you must have covered all of the complications that we have discussed so far. The complications that we have discussed are some of the most common ones, that students are expected to come across.

It is important to understand that consolidation is an advanced and complex topic so you will need to practice as many questions as possible to gain mastery over this topic.