In the past articles we looked at the details of consolidation and its related complications. We have looked at the statement of financial position in detail and now we are going to look at the statement of comprehensive income.

The complications and adjustments will follow the same rationale and calculations, so in that aspect this article will also serve as revision but there are going to be some new things to learn as well because SOCI will deal with the complications in a slightly different manner as compared to SOFP.

With SOCI the main problem relates to reporting the profit or loss for the period and therefore this article is going to focus on items of profit or loss. The consolidated statement of comprehensive income, in a manner like the balance sheet merges all items of income and expenditure of the parent and the subsidiary. It is a straight cross cast of equivalent items.

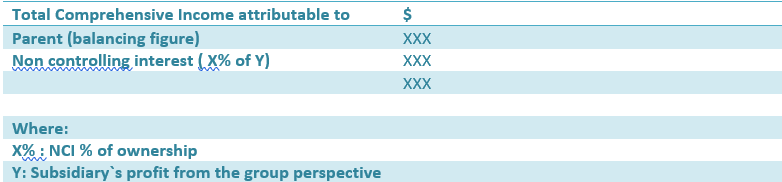

Disclosure of Non-Controlling Interest in Income Statement

The amounts attributable to the owners of the group and the NCI are shown as a small table directly below the Income Statement in the books in the following format.

Pre and Post Acquisition Profits

If you recall the earlier articles, you will remember that according to IFRS 10 we only consolidate post acquisition profits. The examples that we discussed so far were simple in nature where a subsidiary was acquired at the end of the financial year.

However in exams and in real life situations, you may come across situations where a subsidiary is acquired during a financial year. In this case the income, expenditure and the profits of the subsidiary will have to be divided into pre and post acquisition profits.

Examination question usually state that the profits accrued evenly throughout the year, in this situation the profits can simply be apportioned based on the number of months to be allocated to pre acquisition profits and post acquisition profits. For instance, if a subsidiary is acquired on 30th June then 6 month profits will be apportioned to pre acquisition profits and 6 month profits will be apportioned to post acquisition profits. So, we will only consolidate the profits that accrued in the six months after the acquisition i-e 1 July to 31st December.

Complications

1. Intercompany trading

Intercompany trading as we have discussed before is common among companies within a group. From an individual company`s perspective it is perfectly fine but for the sake of consolidation these transactions need to be cancelled.

For the Income statement, the complete transaction value needs to be eliminated from view of the group. Let us look at a simple example.

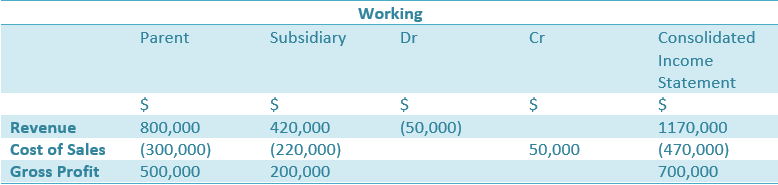

Example 1

P acquired 80% of S. During the year P sold goods worth $ 50,000 to S, by the end of the year S had sold all of the goods bought from P and did not have them in stock.

The adjustment for intercompany trading will be as follows. Only the value of intercompany sale will have to be eliminated regardless of the fact that whether it is in stock or sold completely. It should be kept in mind that only intercompany sales should be eliminated, sales by either the parent or subsidiary made outside the group is perfectly fine from the individual and group point of view.

It can be seen that while the individual statements of the parent and subsidiary remained the same, we had to remove the intercompany transaction from the consolidated statements in order to show the transactions at their fair value to the group and prevent inflation of revenue figures. The gross profit however remained the same because the elimination of the transaction from sales and cost of sales countered each other and created Zero effect.

Now let us add another complication to this by introducing unsold inventory. As we have discussed before, the unsold items of inventory must be shown at the lower of cost or net realizable value as per IAS 2.

The adjustment for unrealized profit is going to reduce the gross profit and ultimately it will affect the group retained earnings and NCI would share the effect if the sale was made by subsidiary. This should not be new information as we have already done this before. Let us now have a look at a simple example.

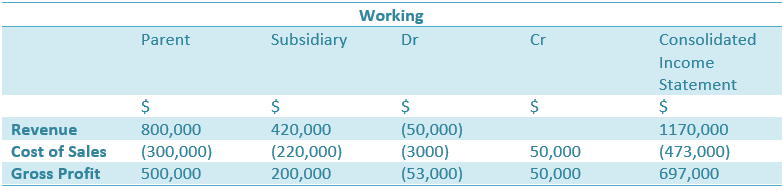

Example 2

P acquired 80% of S. During the year P sold goods worth $ 50,000 to S at markup on cost. By the year end S still had goods worth $15000 which had a total mark up of $3000.

The adjustment for intercompany trading will be the same as above. Only the value of intercompany sale will have to be eliminated regardless of the fact that whether it is in stock or sold completely. It should once again be kept in mind that only intercompany sales should be eliminated, sales by either the parent or subsidiary made outside the group is perfectly fine from the individual and group point of view.

Next we will need to make adjustment for the unrealized profit that is $3000. For the adjustment the closing inventory of the group needs to be reduced by $3000 to show it at the lower of cost or NRV. In order to reduce closing inventory we will need to debit cost of sales.

Point to remember

• Adjustment for Intercompany trading has nil effect on gross profit

• Adjustment for unrealized profit reduced gross profit for the group.

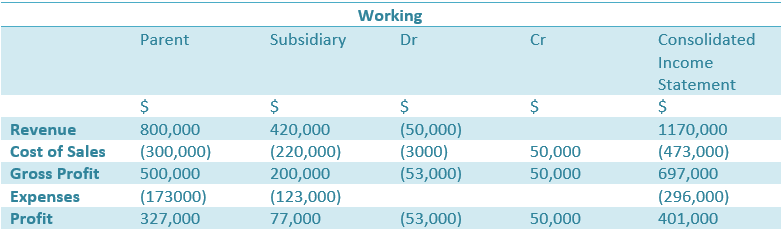

Now let us look at example 3 with the same data but this time the goods were sold by S to P.

Example 3

P acquired 80% of S. During the year S sold goods worth $ 50,000 to P at markup on cost. By the year end P still had goods worth $15000 which had a total mark up of $3000.

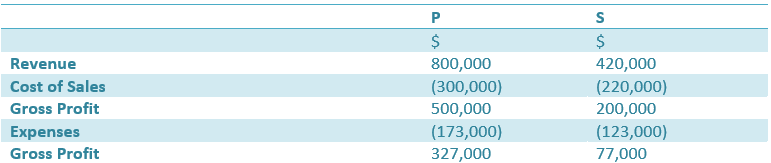

Following data is available

The adjustment for intercompany trading will be the same as above. Only the value of Intercompany sale will have to be eliminated.

Next we will need to make adjustment for the unrealized profit that is $3000. For the adjustment the closing inventory of the group needs to be reduced by $3000 to show it at the lower of cost or NRV. In order to reduce closing inventory we will need to debit cost of sales. But the added complication here is that the sale was made by the subsidiary which means that NCI will also have to share in the adjustment.

The unrealized profit is $3000 and 20% of $3000 is $600, this is the figure that will be deducted from NCI`s share.

Now we need to determine the share of NCI.

Profit of the subsidiary is $77000 but from the group`s perspective, this should be reduced by $3000 because of unrealized profit so it will be $74000 from the group`s perspective.

NCI share: $74000 x 20% = $14800

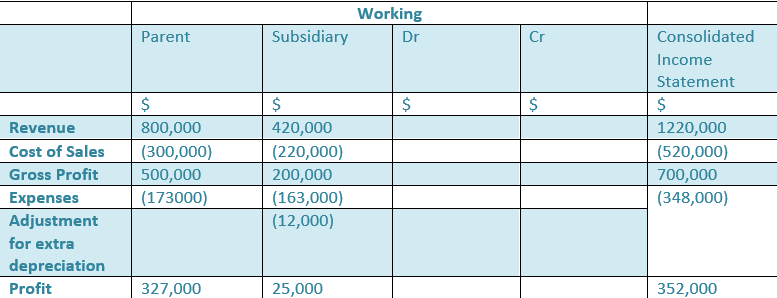

Fair value adjustments

If the value of an asset is revalued, then the Income statement will take the effect of extra depreciation in case of upward revaluation. If the asset belonged to the parent then the extra depreciation will happen in the books of the parent and therefore the ultimate effect will be on the parents share of retained earnings. Whereas if the asset belonged to the subsidiary, then the adjustment will take place in the books of the subsidiary and this will then have an effect on the share of NCI.

Example 4

Assume that P acquired 80% stake in S and on the date of acquisition, S had a depreciable asset with a fair value that was $120,000 in excess of its book value on that date. The extra depreciation for the year on this asset amounts to $12000.

NCI share

Impairment of Goodwill

Impairment in the value of purchased goodwill has no impact on the individual parent or subsidiary books, it only affects the consolidated income statement and balance sheet.

• In the SOFP, the value of goodwill is reduced by the amount of impairment.

• In the SOCI. the impairment expense is charged which reduces the group consolidated profit.

Intercompany management fee, interest, and dividend

It must be reiterated that all intercompany transactions and balances need to be eliminated including but not limited to management fees, or interest paid within the group and dividends paid by the subsidiary to the parent.

Dividends are not included because they are already included in the profit out of which they are paid from. So there is no point in including the dividends again, that`ll simply inflate the retained earnings of the parent.

Conclusion

With this article, we have therefore completed our series of articles on consolidation of group financial statements. You may find that this is not a complete guide because still there are many consolidation related issues that we couldn`t discuss in this series but we have tried to cover the general understanding behind consolidation and some of the most common complications that arise during consolidation. I hope you found this series helpful for you as you might already got 70%-75% of the overall knowledge in this series. Please continue reading and exploring other topics in the same subject.