Consolidation of

Financial Statements|

Part 4

In this article we are going to continue looking at some of the complications that arise during consolidation of group financial statements. In the previous article we looked in detail at the treatment of unrealized profit on inter group trading. Do have a look at it if you haven`t done so far.

Consolidation Complications

Now that you have fully understood how to account for unrealized profit, it must be noted that when we carry out adjustments to settle the complications that arise during consolidation, we have to be careful about the effect on four items.

• Group retained earnings

• Parents profit

• Subsidiary profit

• Non-controlling interest

Most of the complications will affect some or all these categories. For instance, if an adjustment only affects the profit of the Parent then it will also affect the group retained earnings but not anything else.

But if an adjustment affects the subsidiary profit, then it will affect both the group retained earnings and the non-controlling interest`s share of profit. This key consideration must be kept in mind while working on complications.

Acquired Intangible Assets

According to IAS 38, internally generated intangible assets cannot be recognized by a company in its balance sheet however if a company is acquired by another company then The acquirer can show the acquired intangible assets in its balance sheet.

For this reason, when a parent acquires any subsidiary that has got internally generated intangible assets then the said asset must be shown in the group financial statements.

For instance for Netflix, the brand Netflix is an internally generated brand that they have created over the years but if Netflix was acquired by another company then for the acquiring company Netflix would be an acquired intangible asset and would therefore under IAS 38 be required to be disclosed on the face of the financial statements.

The adjustment for the acquired intangible assets is quite simple.

• The recognition of acquired intangible asset will require the parent to adjust the net asset value first and foremost. The net asset value will simply need to be increased by the amount of the acquired intangible asset. So, for instance if the net asset value of a subsidiary was $1 million before the inclusion of acquired intangible asset valued at $100,000. Then the new net asset value would become $1.1 million.

• If you have followed out previous articles, you can guess the next effect. If the net asset value has been revised upwards, then this means that it will also affect the goodwill calculation.

• Another impact of increase in net asset value at the date of acquisition will go to the share of NCI at acquisition, this will also go up.

• The next adjustment for this will be the year end value of the brand. the brand will need to be amortized and this extra amortization will reduce the post-acquisition earnings of the subsidiary in the groups books.

• The result of reduction in post-acquisition earnings of the subsidiary in the groups books will be that the share of parent and NCI from the post acquisition earnings of the subsidiary will be reduced.

Let us now look at this with a simple example before moving on.

Example 1

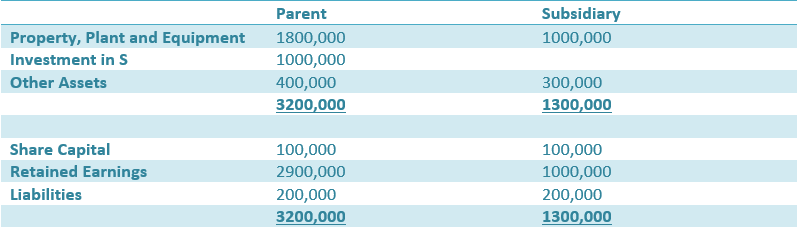

Suppose P bought 80% stake in S, 2 years ago.

At the date of acquisition the retained earnings of S were $600,000. The fair value of the net assets was not materially different from the book value of the net assets except for the internally generated brand, which was not recognized by S. The fair value of this brand is expected to be $100,000 at the date of acquisition and it has a remaining life of 20 years.

The following information is also available.

Now we are supposed to prepare a consolidated statement of financial position. At this point you should recall the steps that we have discussed in the path. Here are the steps once again for your revision.

• Firstly, follow the preliminary steps that we have already discussed.

o Step 1: Identify the types of entities in the group - In this group we have got a parent and a subsidiary

o Step 2: Identify the date of acquisition and the date of consolidation - Difference between both dates is of 2 years

o Step 3: Identify the consideration paid - The cost of acquisition is $1000,000

o Step 4: Identify Non-Controlling Interest at acquisition - Needed to be calculated

o Step 5: Identify goodwill at acquisition - Needed to be calculated

• Secondly, consolidate the statements

• Thirdly, calculate the value of retained earnings and NCI at the date of consolidation.

First we need to carry out simple calculations related to goodwill, NCI and retained earnings but before we can get started with these calculations we will need to find out the correct value of net assets at acquisition and consolidation.

Technique for simplifying the net assets calculation

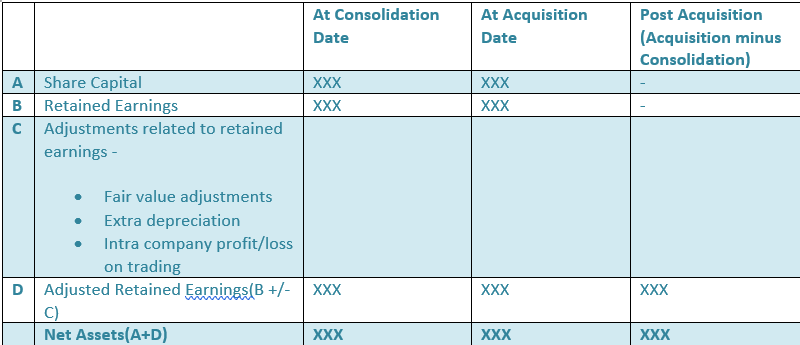

Net asset calculation at the date of acquisition and at the date of consolidation is a major part of consolidation questions. There is a technique that you can use to simplify this calculation. By all means you can separately calculate net assets of the subsidiary on the date of acquisition and consolidation but doing so will take a lot of time.

Alternatively, you can follow this method to calculate the figures quickly.

At first look this table may look complicated but if you take a second look then this is simply the equity and reserves section of the subsidiary. This table is a very simple one, you may also have share premium and other reserves in real life examples. However if you are student then examination questions even at professional level examinations will hardly be more complex than this.

The share capital figure remains the same usually on the dates of acquisition and consolidation. The major adjustments will only be required under the retained earnings figure. Once again the retained earnings figure on the date of acquisition will usually be same and will rarely require any adjustment. If it does, you can simply add or subtract the required change.

It is the figure on the date of consolidation that we are more concerned about because all of the complications that we have discussed so far will require adjustments in the retained earnings on the consolidation date.

At Consolidation Date At Acquisition Date Post Acquisition (Acquisition minus Consolidation)

By making this table in your working, you can neatly make all the adjustments to the retained earnings figure of the subsidiary. The adjusted retained earnings figure is the figure that we are looking to calculate.

Once you have calculated it, you can move on to complete the table.

Adding up the share capital and the adjusted retained earnings figure will give the figure for net assets at acquisition and consolidation.

The third column is basically the difference of the second and first columns. Third column makes it simple to get the figure for post acquisition profit of the subsidiary, if you recall this figure is used to calculate the share of profit for NCI and parent.

We can understand this better if we continue our example.

It is therefore advisable to use the following working format, as it makes it simple to calculate the net assets at acquisition and consolidation, as well as the post-acquisition profit of subsidiary with ease.

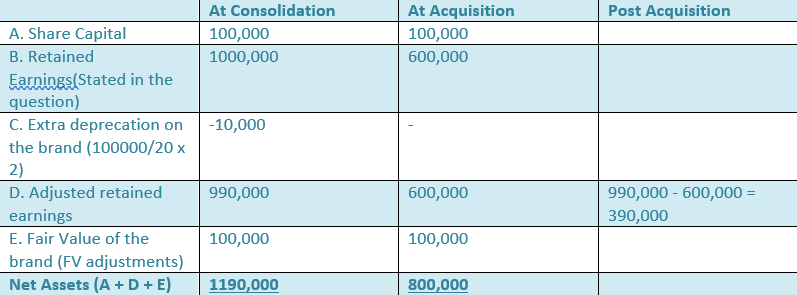

Can you see how easy it is to calculate the required values in this manner. Retained earnings at acquisition do not need to be adjusted but the earnings at consolidation date need to be adjusted for depreciation. In addition to this we need to recognize the brand and doing so will increase the net asset value of the company. So this is a very straight forward adjustment.

From this point it is simple to calculate the other figures.

NCI Calculation

This calculation is for the final figure for Non Controlling Interest that will show up in the statement of financial position. So far we have discussed NCI in bits and pieces and now that we are in the advanced stages of this topic, it is better to bring together those bits and pieces of understanding to formulate a complete picture.

The figure for NCI in the balance sheet comprises of the following items

• Share of net assets on the date of acquisition (Usually given in the question)

• Share of post acquisition profit of the subsidiary (Retained profit at acquisition minus adjusted retained profit at consolidation, look at the third column of the table for this figure)

Both of these shares can be found out simply by applying the percentage of NCI to the relevant figures. If you look at the table above, then you can see that we have already calculated the figures for net assets and post acquisition profit, so we simply need to apply the percentages to calculate the final figure for NCI.

Share of assets at the date of acquisition (20% x 800000) 160000

share of post acquisition retained earnings(20% x 390000) 78000

NCI figure to be included in SOFP 238000

There is a quicker way to calculate the NCI figure, you can also use it to check if you are doing it right or wrong. Simply take the net assets figure on the date of consolidation. In the above example this figure is $1190,000 and apply the NCI percentage on it.

So,

1190,000 x 20/100 = $238,000

The answer you can see is the same. So unless you are attempting a consolidation question in the exam where you are required to show the working in steps, you can simply apply the percentage on the net assets figure on the date of consolidation in order to quickly find out the final value of NCI that should be included in the statement of financial position.

Goodwill Calculation

We have done this in previous articles. IFRS 3 gives out the following simple formula for calculating goodwill upon acquisition

We simply have to plug in the figures into the formula.

Consolidated/Group retained earnings

This is the final figure for Consolidated or group retained earnings that will appear in the statement of financial position. This final figure comprises of all of the retained earnings of the parent after adjustment and the parents share of subsidiary`s retained earnings after adjustments.

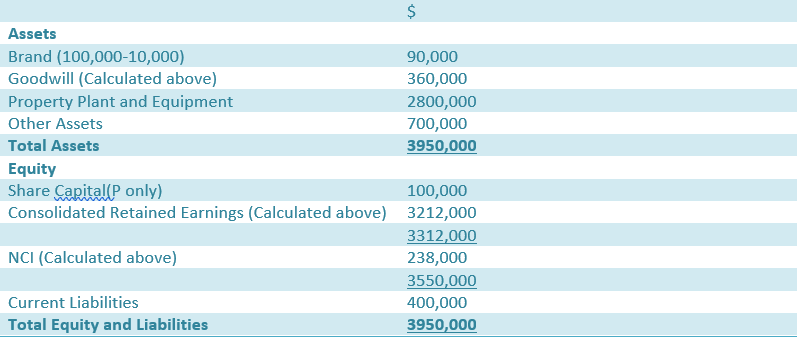

Once you have calculated the required figures, creating the SOFP is simply a matter of plugging them into the SOFP format.

Group Consolidated Statement of Financial Position,

As at 31 December 20x0

Hopefully you have understood how to account for acquired intangible assets. Now we shall move on to another area of complications that arise during consolidation.

Fair Value Adjustments

IFRS 3 requires all assets to be measured at their fair value at the time of acquisition. A scenario may include the assets of a subsidiary being revalued upwards or downwards and therefore there will be a need to revalue the assets in the books of the subsidiary before consolidating them.

The calculation for revaluation adjustments is similar to the acquired intangible assets adjustments. So let us directly look at an example to understand it in a better manner.

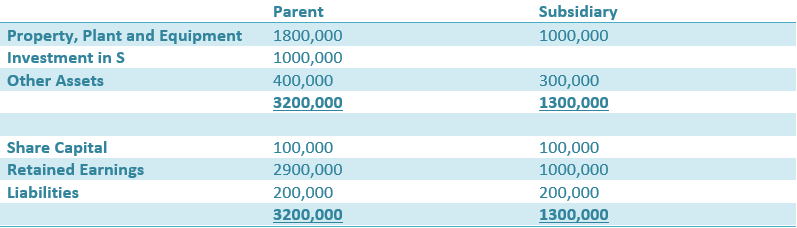

Example 2

Assume that P bought 80% of S, 2 years ago and on the date of acquisition, the retained earnings of S were $600,000 with the fair value of net assets at $1000,000. It was noted that the fair value was higher than the net book value of assets by $300,000. The purchase price paid for this investment was 1000,000

This difference in value was due to the revaluation of an asset with a useful economic life of 10 years.

The following information is also available

So the question makes it clear that there is a $300,000 upwards revaluation. Our method of working will be similar.

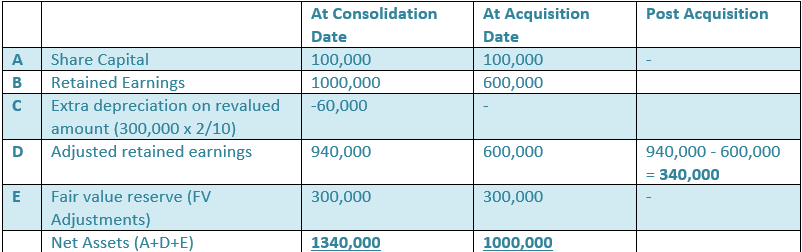

• Firstly calculate the net asset value at the date of acquisition and consolidation while taking the effect of revaluation.

• Calculate the NCI, Goodwill and Group retained earnings.

This is the same table that we did in the earlier example. In this example you can see that an additional item "Fair value reserve" has been added. This has been added because as you can understand, upward valuation of the assets, increased the net asset value of the business, so in order to account for this increase in net asset value, we have added a fair value reserve.

Non controlling Interest

If you have followed the above mentioned example then it should be clear where the figures in this table are coming from, if you are still not clear then spend some more time on the first example.

Goodwill

Consolidated/Group Retained Earnings

Property Plant and Equipment

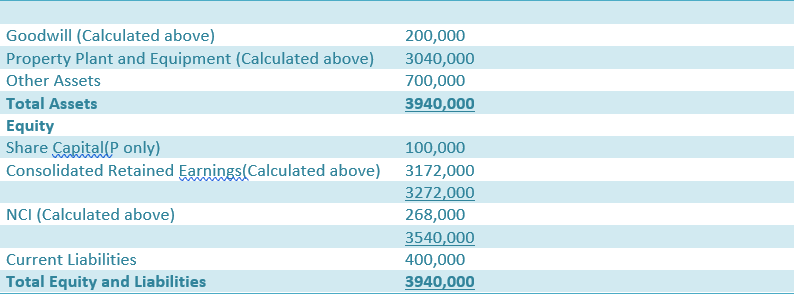

Since there have been adjustments into the property Plants and equipment due to revaluations, we will also need to calculate its figure.

Now we simply need to plug in the figures into the balance sheet.

Group Consolidated Statement of Financial Position,

As at 31 December 20x0

So you see the calculation for revaluations is similar to acquired intangible assets. The key point for solving consolidation related questions is to remember the flow of working. Once you remember the effect of each adjustment and the flow, you will not have any trouble with consolidation.