Consolidation of

Financial Statements |

Part 2

In the last article we went through the introduction of consolidation of group financial statements and touched the considerably basic definitions and preliminary steps. In this article we are going to pick up from where we left and try to learn some new concepts.

Let us go over the preliminary steps once again, just for revision.

• Step 1: Identify the types of entities in the group

• Step 2: Identify the date of acquisition and the date of consolidation

• Step 3: Identify the consideration paid

• Step 4: Identify Non-Controlling Interest at acquisition

• Step 5: Identify goodwill at acquisition

Hopefully, you`ll remember these steps. If you need to revise you can look at the previous article. We shall begin this article by looking at the last two steps in greater detail by going over some worked examples, just to make sure that the concepts are laid out clearly.

The process of calculation of goodwill and non-controlling interest is a rather complex one for beginner level IFRS students/ professionals, therefore it is especially important to get this cleared as early as possible before moving on wards. So let us look at an example.

Example 1

Company X acquired Company Z on 31st December 2019. X bought 4 million shares out of a total of 5 million shares of Z. The consideration that amounted to $10 million, was paid in cash by X to Z. On the date of acquisition, the fair value of all the assets of Z was $7.5 million.

Calculate the goodwill and non-controlling interest at acquisition. Assume that the group policy is to value NCI at the proportionate value of the fair value of assets.

The question is noticeably clear, now if you get confused there is no need to get worried. Simply remember the preliminary steps and complete them in the order that we have discussed.

Step 1: Identify the types of entities in the group

In this group there are 2 entities. Company X and Company Z. Company X has acquired 4 million out of 5 million shares. This means that X now controls 80% of Z, which makes company X the parent of company Z, which is a subsidiary. So the controlling stake is 80%.

Step2: Identify the date of acquisition and consolidation.

It is immaterial in this question as we are not carrying out a complete consolidation. But still for clarity the date of acquisition is 31srt December 2019 and the date of consolidation is not mentioned. Usually it is one year after the acquisition, but it can be an interim date as well.

Step 3: Identify the consideration paid.

This has been stated clearly in the question as $10 million.

Step 4: Identify Non-Controlling Interest at acquisition

Now, this is where it gets interesting. The question states that the group policy is to value NCI at the proportionate value of the fair value of net assets. Now before we continue, let us look at the definition of NCI.

IAS 27 defines non-controlling interest as " the equity in a subsidiary not attributable, directly or indirectly, to a parent". Previous versions of this standard termed non-controlling interest as minority interest.

So, what this means is that whatever portion of the company is not owned by the parent, that is called non-controlling interest. In the example Company X owns 80% of the stake in company Z and this means that 20% of the remaining stake is non controlling interest.

Now the question has asked for valuing NCI at the proportionate value of fair assets.

It should be easy from here. The fair value of the assets of company Z stated in the question is $7.5 million. This means that 20% of $7.5 million belongs to the NCI.

20% x $7.5 million = $1.5 million.

According to the proportionate value method, this is the amount of NCI at acquisition. Once we have found NCI at acquisition, calculating the goodwill is simply a matter of plugging in the values in the format.

Step 5: Calculate the value of Goodwill

That was simple right.

Now sometimes, the company policy may be different and a company may decide to value NCI at full value or on fair value. So we shall have the same question but with a different requirement.

Example 2

Company X acquired Company Z on 31st December 2019. X bought 4 million shares out of a total of 5 million shares of Z. The consideration that amounted to $10 million, was paid in cash by X to Z. On the date of acquisition, the fair value of all of the assets of Z was $7.5 million. The market value of shares at the time of acquisition was $2 per share.

Calculate the goodwill and non-controlling interest at acquisition. Assume that the group policy is to value NCI at fair value.

Steps 1, 2 and 3 will remain the same.

There will be no difference in them. But things will be different in steps 4 and 5. So let us have a look.

Step 4: Identify Non-Controlling Interest at acquisition.

Now the question asks us to calculate NCI at fair value. This means that we cannot use the proportionate value method. The question stated that the market value of shares is $2, and 1 million shares are non-controlling interest.

We can easily apply $2 to 1 million shares to arrive at the $2 million fair value of NCI.

Step 5: Calculate the value of Goodwill

From this point, it is only a matter of plugging the values.

Let us now compare the outcome of two methods to understand the effect of both methods.

It can be clearly seen that the proportionate value method gives a lower value compared to the fair value method, this is also why the fair value method is also known as the full value method.

Now that we have looked at the preliminary steps of consolidating a group financial statement. Let us now look at the finer details of consolidation. Consolidated statements are prepared so that they can have meaning for the stakeholders and users of financial statements. IFRS10 requires subsidiaries to be consolidated with the parents whereas associates are not consolidated.

The reason for this is that although all the companies within the group are separate financial entities but in practice they operate as if they are one organization. Therefore, the purpose of consolidating is to represent the substance of the situation, as the group is effectively a single economic unit.

Steps of Consolidation

To make any question or scenario on consolidation easier, you may want to follow the following steps. You may not find this in any book as this is a personal technique that I have used over the years and these steps help simplify the calculations.

• Firstly, follow the preliminary steps that we have already discussed.

• Secondly, consolidate the statements (we will discuss this in this and future articles)

• Thirdly, calculate the value of retained earnings and NCI at the date of consolidation.

The first two steps should be easy but most IFRS students/ professionals face difficulties in the final step when they are required to calculate the closing figures for retained earnings and NCI.

You may not know how to carry out all these steps, do not worry because we are going to cover all of the fine details in this series of articles.

How to Consolidate

• The assets and liabilities of both the parents and the subsidiaries should be combined in a single consolidated statement of financial position.

• The profits of the parents and the subsidiaries should also be combined in the consolidated statement of comprehensive income.

Consolidating the Statement of Financial Position

As we have mentioned it multiple times before, consolidation requires merging the financial statements of the parents and subsidiaries. Let us start with the statement of financial position as it is considered by IFRS students/ professionals as generally easier to understand.

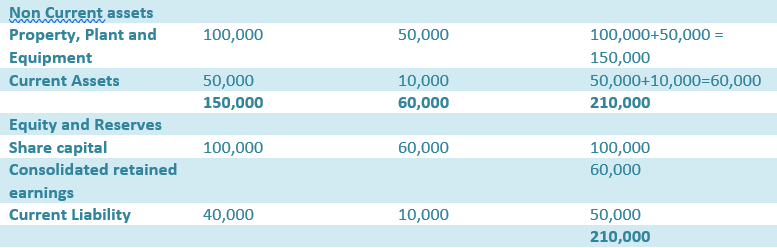

The theory of consolidation is simple. You take the SOFP of the parent and the subsidiary, list down all the assets and liabilities in a new consolidated SOFP line by line, as you would do normally and then simply add the same assets together and transfer them to the consolidated SOFP.

Here is a quite simple example to give you an idea.

In this very simple example you have seen that the assets and liabilities have been consolidated simply by adding together. However in the equity and reserves section you will notice that we did not add the share capital of the two companies together.

The consolidated statement only shows the equity of the parent company and not the subsidiary. Ignore the consolidated retained earnings for now because we are going to look at that in detail later.

Hopefully you have got the basic idea of consolidation clear in your mind. Most of the times, consolidating the SOFP will simply require adding the figures together. However there will be scenarios where more complex knowledge and expertise will be required.

For instance some of the complications that may arise on consolidation are

• Recognition of intangible assets such as goodwill and brands etc. Internally generated intangible assets cannot be recognized in the books of the entity that owns them but in the case of an acquisition the parent entity must show them in the consolidated statements. In such a scenario, acquired intangible assets may also have amortization charged on them and therefore this calculation will affect the retained profits.

So adjusting for this transaction will require recognizing the effect in assets and retained profit.

• Fair value exercise at acquisition is also a common practice. The assets of the subsidiary may be revalued on the date of acquisition and therefore the effect of revaluation and the subsequent depreciation needs to be reflected in the non-current assets, retained profit and in turn the NCI.

• Cancellation of intra group transactions. Parents and subsidiaries usually engage in transactions with each other and all such transactions need to be eliminated as if they did not occur, their effect needs to be removed from the consolidated statements and this will therefore require a simple reversal of the relevant transaction. But doing so may affect the retained earnings.

IFRS 10 requires that all intra group balances, income, expenses and dividends must be eliminated and profits/losses resulting from intra group trading in inventory or non-current assets must be eliminated.

Feeling confused? Apprehensive? Calm down because we are going to cover all these things in detail in the coming articles and as we progress you will see that these complexities will start to feel easier with time.